Between Reversals and Persistence of Trends

Best/Worst Performance DEC 2025

The contrast between November and December 2025 revealed a market that, far from following a linear trajectory, preferred to dance between unexpected reversals and the tenacious confirmation of underlying dynamics.

While November recorded a month of volatility characterized by defined winners and losers, December brought a different narrative: the correction of excesses and the continued punishment of previously penalized positions.

December’s Paradox: Less Corporate Performance, Better Personal Results

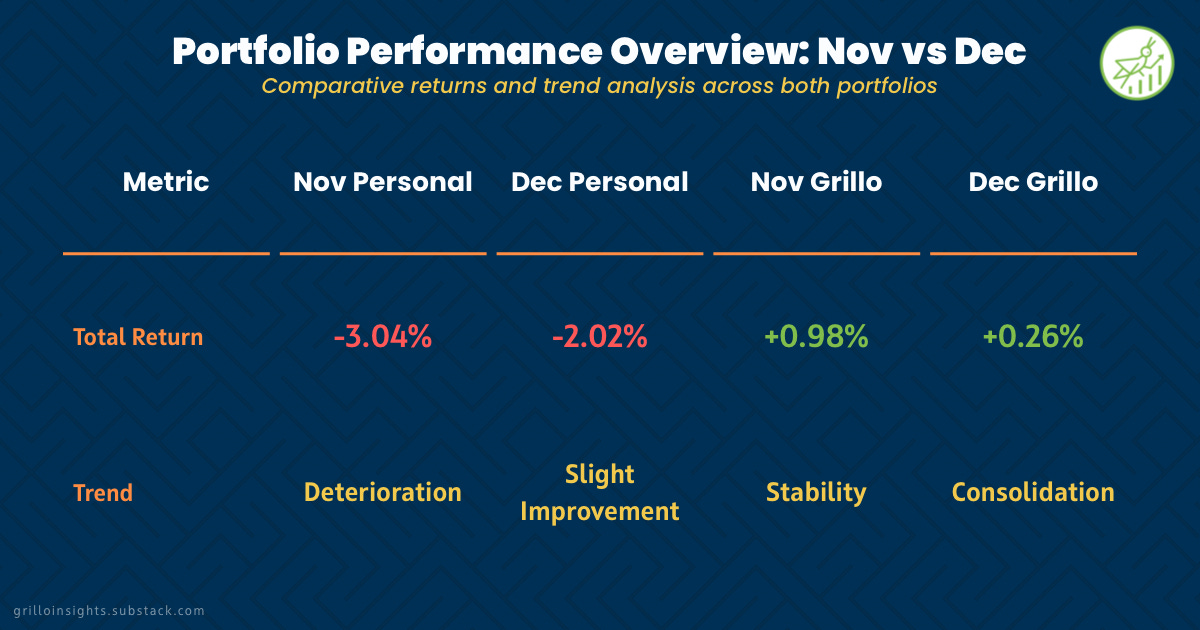

December’s most intriguing contrast manifests in aggregate returns.

The Grillo Technologies corporate portfolio achieved a modest +0.26%, barely improving on its November result (+0.98%), while the personal portfolio experienced a decline of -2.02%, compared to -3.04% in November.

In absolute terms, both portfolios closed December in negative or stagnant territory, but the nature of this weakness was radically different.

November was a month where concentration in extraordinary winners (Google +13.59% personal) broadly compensated for losses. December, in contrast, was a month of alignment: both winners and losers in the personal portfolio converged toward the market median, suggesting that the previous month’s excesses corrected in a relatively orderly fashion.

The Best: The Market Changes Narrative

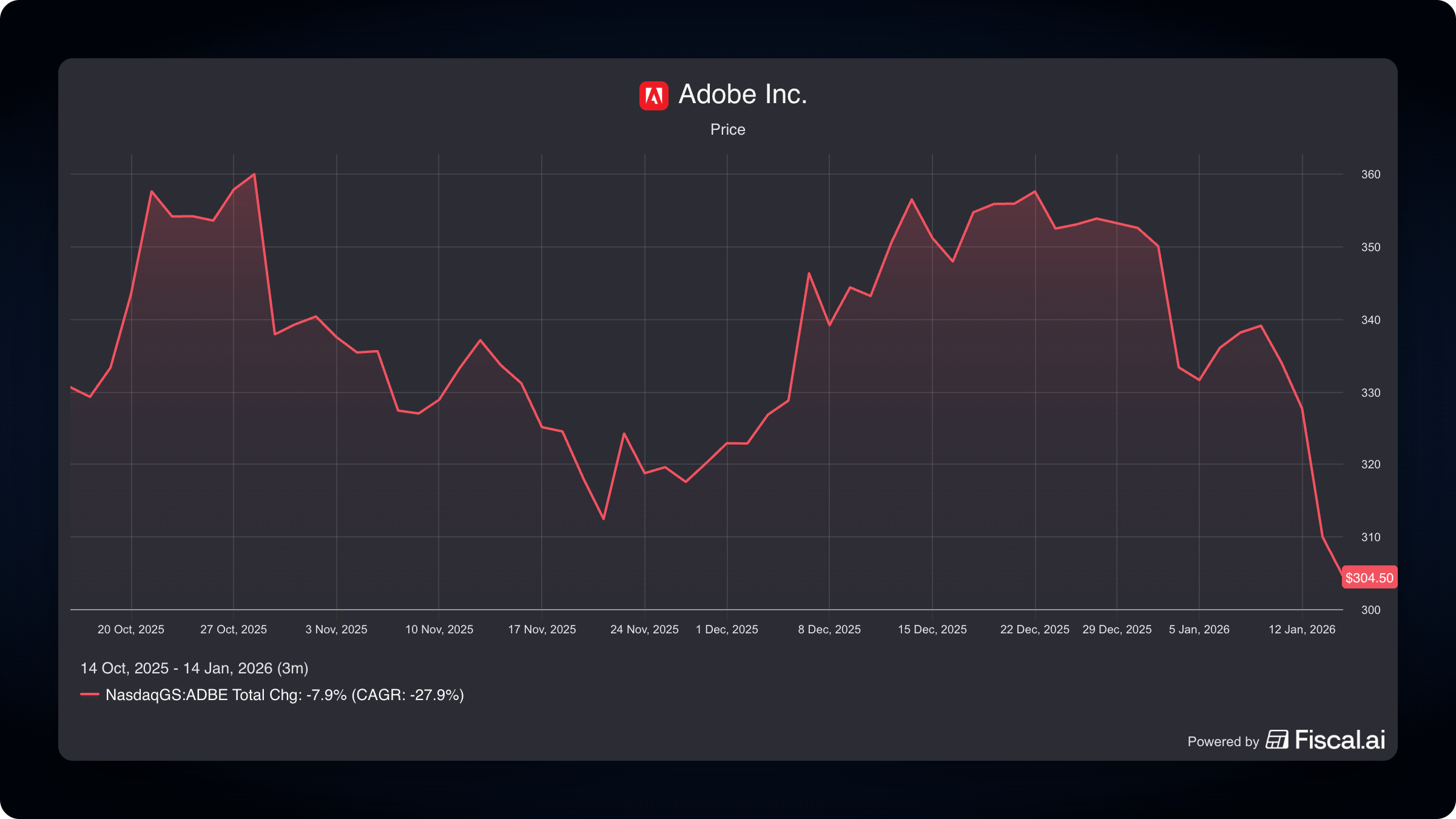

Adobe: From Ostracism to Rehabilitation

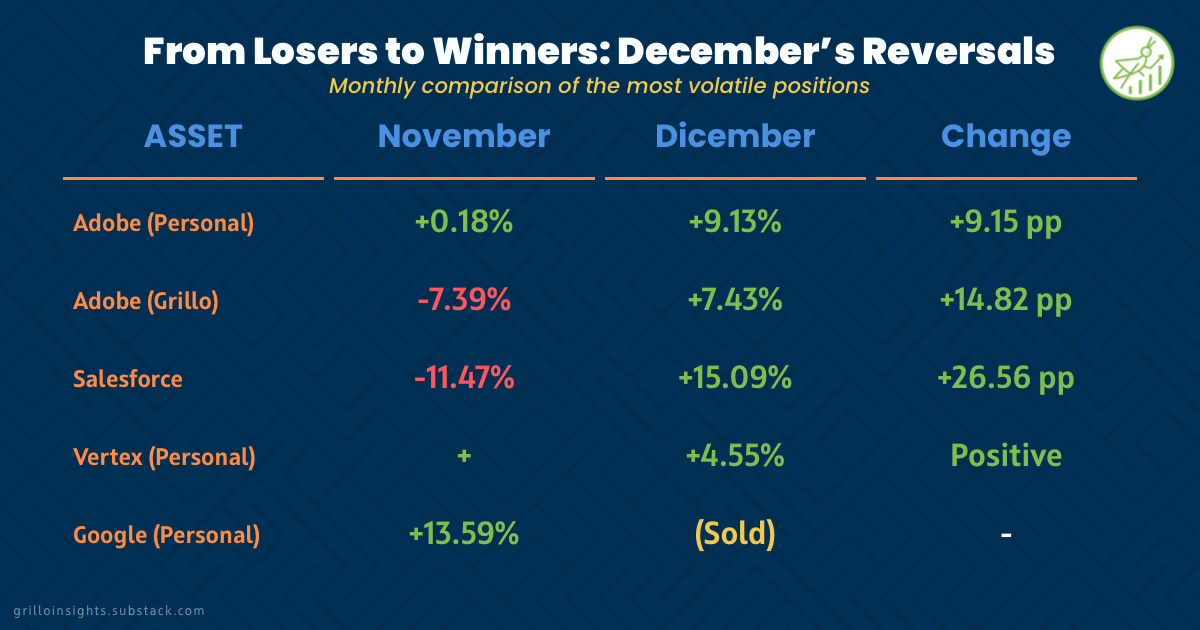

Adobe ADBE 0.00%↑ represented perhaps the most dramatic reversal between both months. In November, the company suffered a -7.39% drop in Grillo Technologies (though it rose marginally +0.18% in the personal portfolio), generating a loss of $23,449.50 MXN in the corporate portfolio. December, however, was cathartic: Adobe recovered all that confidence and more, with a return of +9.33% in the personal portfolio and +7.43% in Grillo Technologies.

What changed? The narrative was less complex than expected. Despite fears about AI competition and internal product cannibalization, investors recognized that Adobe maintains extraordinary pricing power and enviably high operating margins.

The decision to buy more after November’s drop (as documented in the previous analysis) was validated, but this points to a critical lesson: technology markets were punishing Adobe for narrative reasons, not fundamental deterioration.

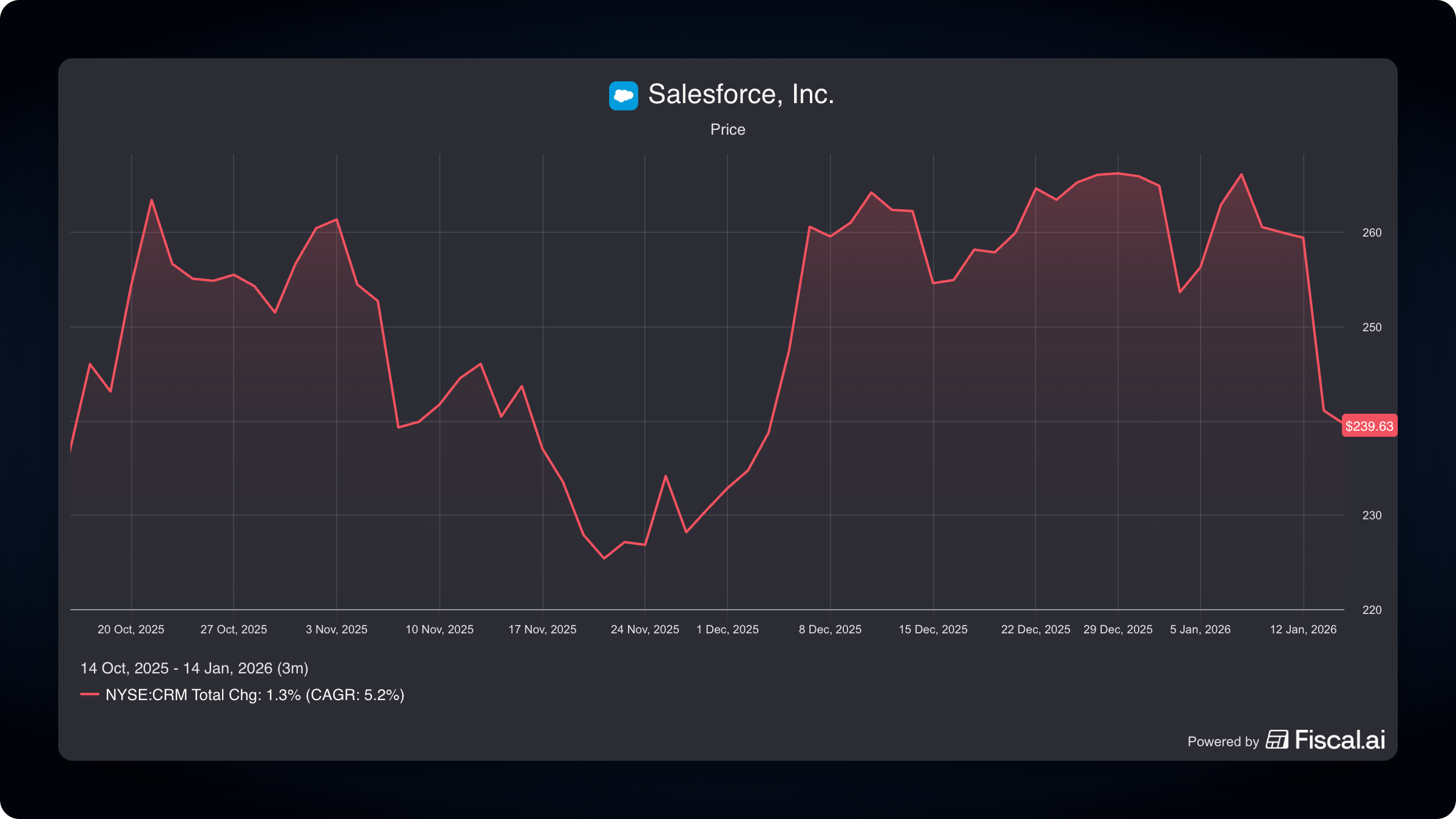

Salesforce: The 180-Degree Reversal

If Adobe was a reversal, Salesforce CRM 0.00%↑ was a categorical turnaround.

In November, the company fell -11.47%, fueling concerns about growth deceleration and margin pressure in a higher-rate environment. December completely reversed that position with a spectacular return of +15.09%.

This change is particularly revealing. November punished Salesforce for legitimate doubts about its ability to execute transformations toward enterprise agents. December forgave, suggesting that markets better absorbed the transformation narrative and recognized that the company has a clear path to justify its valuation.

With a Forward P/E of 25.3 noted in November, Salesforce appears to be in the territory where proven execution matters more than the risk narrative again.

Vertex Pharmaceuticals: The Consistency of Fundamentals

Vertex VRTX 0.00%↑ demonstrated remarkable consistency between both months.

In November it generated positive returns, and in December continued with a return of +4.55% in the personal portfolio and +2.78% in Grillo Technologies.

Its gene editing technology and portfolio of cystic fibrosis medications maintain robust underlying demand that markets didn’t significantly punish at any point.

The Worst: When Gravity Persists

TransMedics: From Success to Catastrophe in Thirty Days

If there’s an example of volatility without clear justification, it’s TransMedics TMDX 0.00%↑ . In November, the company experienced a return of +11.23%, fueling optimism about its organ preservation technology. December was devastating: -16.85%, the steepest drop in the personal portfolio for the month. In thirty days, TransMedics went from being a narrative success to a failure.

What happened? Here manifests the brutal reality of small stocks in medical innovation spaces.

Bearish revisions can be precipitated by clinical data, regulatory changes, or simply by market fatigue with the theme. With a weighted position in the personal portfolio (~$9,245), this drop significantly hurt.

PayPal: The Persistence of Suffering

PayPal PYPL 0.00%↑ offers a different lesson. In November, it fell -9.30%, driven by doubts about its ability to grow in a fragmented digital payments market. In December, it continued suffering with an additional -6.88% drop. This isn’t a reversal; it’s a trend. The market simply doesn’t believe in the recovery thesis, at least not in the short term.

PayPal was the biggest negative learning from the November analysis, where it was recognized that “the market simply doesn’t believe” in the thesis. December confirmed that assessment. With a Forward P/E of 11x noted previously, the valuation is cheap, but the open question remains: cheap for a reason or out of complacency? Markets suggest the latter.

MINISO: Sustained Pressure from China

MINISO MNSO 0.00%↑ fell -6.76% in November and continued falling -5.64% in December. This reflects a broader narrative: exposure to China, even through smaller companies with positive operating flows, remains under pressure.

Yuan devaluation, doubts about international expansion, and political uncertainty maintain negative sentiment.

Corporate Dynamics: Less Drama, More Discipline

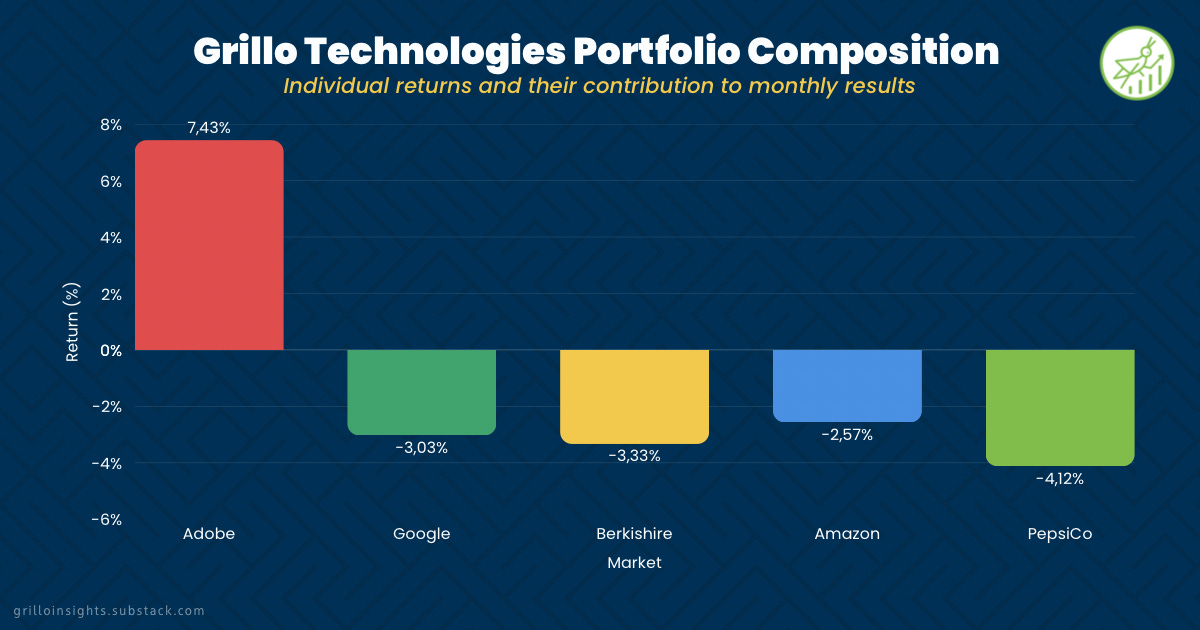

Grillo Technologies experienced a calmer month in December compared to November. While November was dominated by Google’s spectacular rise (+11.79%) and its outsized impact on the portfolio, December was more balanced, with modest gains distributed among Adobe (+7.43%), Visa (+4.18%), and Elevance Health (+4.51%), partially offset by drops in Berkshire Hathaway (-3.33%), Google (-3.03%), and Amazon (-2.57%).

This more balanced distribution suggests that Grillo Technologies wasn’t exposed in a concentrated manner to the more dramatic reversals that punished the personal portfolio. Berkshire and Google fell in December, but their weights in the corporate portfolio didn’t amplify the impact. This is a reminder of an elementary truth: diversification doesn’t generate extraordinary returns, but it cushions them when adversity arrives.

Reflections: Lessons from Two Contradictory Months

November and December together reveal a critical pattern that investors should internalize: markets in 2025 are exhibiting mean-reversion volatility rather than trending volatility. This means that extraordinary gains (Google +13.59%) are frequently followed by corrections (Google -3.03%), and initial drops (Adobe -7.39% in Grillo, Salesforce -11.47%) are usually followed by recoveries (Adobe +7.43%, Salesforce +15.09%).

For the disciplined investor, this presents both opportunities and traps:

The Trap: Extracting causality from temporal correlation. Adobe falling after rising doesn’t mean the initial investment was wrong; it simply means markets corrected excess.

The Opportunity: Recognizing that companies with solid fundamental quality (high margins, robust cash flows, competitive moats) tend to recover after narrative drops. Adobe, Salesforce, and Vertex exemplified this in December.

The Lesson: Extremely concentrated positions in narrative winners (like Google in November) amplify both victories and defeats. December was a month where that amplification worked against the personal portfolio.

TransMedics and PayPal offer a counter-lesson: not every drop is a buying opportunity. When the narrative changes fundamentally (as appears to be the case with PayPal), patience can be more valuable than dollar-cost averaging.

Toward a More Conscious Balance

December 2025 ended up being a month of “correction volatility” rather than “breakout volatility.”

The dramatic reversals suggest that markets are adjusting positions based on excessive interpretation of month-to-month narratives, rather than revaluing fundamental theses. This is relatively healthy for diversified portfolios like Grillo Technologies, but dangerous for concentrated portfolios.

For January 2026 and the months ahead, the clear lesson is that purchase decisions should be based less on short-term momentum and more on companies’ proven ability to generate sustainable cash flows and grow margins. Adobe, Vertex, and Salesforce demonstrated this in December.

PayPal, MINISO, and TransMedics are reminders that when the market simply loses faith, valuation cheapness doesn’t matter. Patience, combined with rigorous evaluation of the durability of each investment thesis, will continue to be the most reliable compass in markets where reversion volatility is the norm.

Disclaimer: This article reflects my personal investment strategy and opinions. I am not a financial advisor. Please do your own research before making any investment decisions.