$PYPL: Strong Numbers, Wrong Time to Change the Captain

Key Metrics for This Analysis:

FY2025 Revenue: $33.2B (+4% YoY, +4% FXN)

FY2025 Transaction Margin Dollars ex-interest: $14.2B (+6% YoY)

FY2025 Non-GAAP EPS: $5.31 (+14% YoY)

Q4 2025 Non-GAAP EPS: $1.23 (+3% YoY; $0.04 below the guided range)

Q4 2025 Total TPV: $475B (+9% spot, +6% FXN)

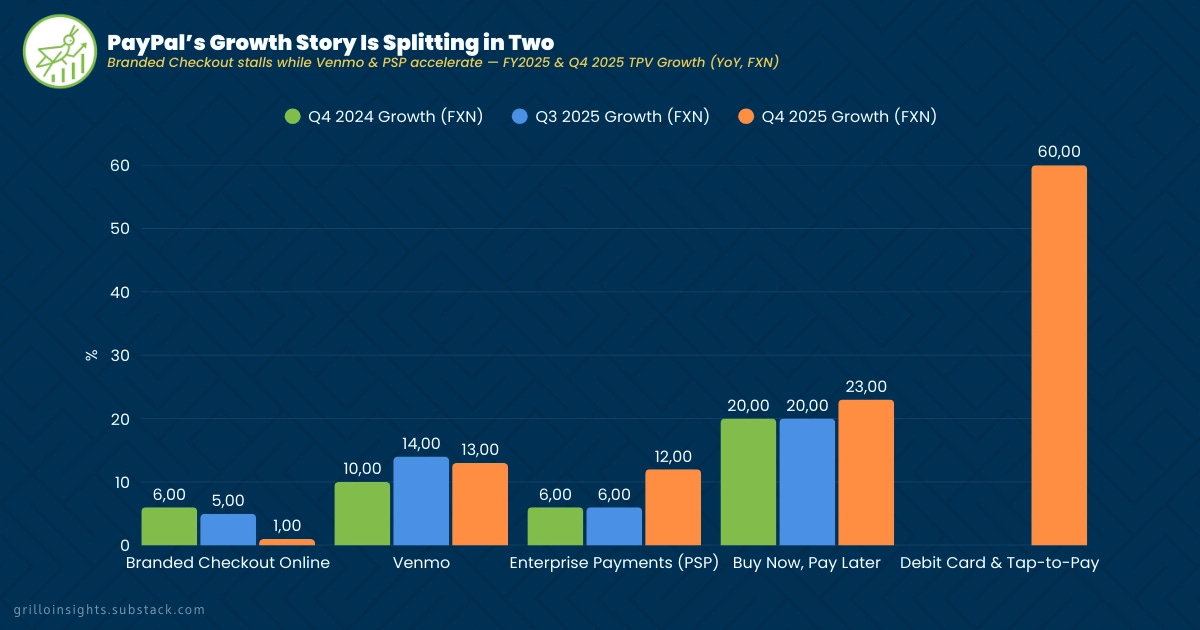

Q4 2025 Online Branded Checkout: +1% FXN (vs. +5% in Q3, +6% in Q4 2024)

FY2025 Venmo Revenue: $1.7B (+20% YoY)

Q4 Enterprise Payments TPV: Double digits (7 consecutive quarters of profitable growth)

FY2025 Adjusted FCF: $6.4B; FY2026 Guidance: ≥$6B

FY2025 Share Buybacks: $6.0B (7% reduction in shares outstanding)

FY2026 Non-GAAP EPS Guidance: Low single-digit decline to slightly positive vs. $5.31

2026 TM Headwind from Strategic Investments: ~3 percentage points

“Checkout-ready” consumers (biometrics/passkey): 36% (+15 pp YoY)

Few companies have held such a prominent place in my investment radar as PayPal. In fact, those who have followed me from the beginning know that the Deep Dive on PYPL 0.00%↑ was practically the one that inaugurated my in-depth analyses.

Back then, my thesis was clear: PayPal was in the middle of a profound transformation, it had unique assets like Venmo and a two-sided network with no real competitor at scale, and the market was underestimating its monetization potential.

Today, after reviewing Q4 and full-year 2025 results, I need to be honest with myself and with you: I sold 40% of my position — I even mentioned it on X. Not because the company is broken, but because the CEO change forces me to reconsider the timeline of my thesis, and that, in a conviction portfolio, has consequences (and I’m sure I wasn’t the only one).

The Numbers Don’t Lie

Let’s start where we always do: the results. And we have to acknowledge that on the surface, 2025 was a good year. Revenue reached $33.2B, growing 4% year-over-year, with Transaction Margin Dollars ex-interest at $14.2B, also +6%.

Full-year Non-GAAP EPS came in at $5.31, a 14% increase, driven in part by an aggressive $6B buyback program that reduced share count by 7%. In Q4 specifically, total TPV reached $475B, growing 9% on a spot basis.

However, if you dig deeper, you start to see the cracks. Q4 EPS was $1.23, coming in $0.04 below the low end of the guided range, hurt by a higher-than-expected tax rate and pressure in branded checkout. Non-GAAP operating margin contracted 9 basis points to 17.9% in the quarter, and revenue growth on an FXN basis was just 3%. These are minor signals, but in a business where market confidence was already being tested, every detail matters.

The Wins That Remain Intact

I remain bullish on several fronts of the business, and I have no regrets about holding the remaining 60% of my position. Venmo was the silent hero of 2025. Its revenue reached $1.7B, growing 20% year-over-year, driven by its evolution into a real commerce platform.

Pay with Venmo TPV grew 32%, and its debit card TPV grew more than 50%. This validates something I said from day one: Venmo had massively underexploited monetization potential, and that process is now materializing.

The Enterprise Payments business (formerly Braintree) is also a success story. Seven consecutive quarters of profitable growth, with TPV accelerating to double digits in Q4. At the start of 2024, they had value-added services they simply weren’t charging for. By the end of 2025, they closed the year with 16 services that merchants are happy to pay for because they improve authorization rates, reduce costs, or mitigate fraud.

This is real pricing power, built with discipline. And the omnichannel strategy is taking its first concrete steps: global debit TPV grew 60% in 2025, and they already have their first enterprise merchant live in physical retail through Verifone — which puts them in the game to compete for the 80% of payments that still happen offline.

The Problem We Can’t Ignore

Here comes the hard part. The financial heart of PayPal — online branded checkout — grew just 1% FXN in Q4, falling dramatically from 5% in Q3 and 6% in the same quarter of the prior year.

Branded checkout represents more than half of the company’s total profit dollars. That 4-point deceleration in a single quarter is exactly the kind of signal that, as a long-term investor, I can’t normalize.

The company attributes the decline to three factors:

Macro weakness in U.S. retail, with lower- and middle-income consumers under pressure (their core demographic)

International headwinds, particularly in Germany

A deceleration in high-growth verticals such as travel, ticketing, and gaming following very strong prior-year comparables

All of that is real. But what concerns me most is the third element that management itself acknowledged with unusual honesty: execution problems. They underestimated the complexity of integrating large merchants, deployed the new checkout experience without activating biometrics in parallel — which negates much of the conversion uplift — and failed to achieve sufficient competitive presentment, meaning PayPal appearing first at the moment of payment.

When both elements are properly implemented, the data is compelling: merchants that during Cyber Five had the modern experience, upstream BNPL, and co-marketing showed double-digit branded TPV growth. The problem is that this only applies to a small fraction of their current merchant base.

The CEO: The Breaking Point of My Thesis

And here we reach the central moment of this note. On February 3, 2026, alongside its results, PayPal announced that Alex Chriss was stepping down and that the board was naming Enrique Lores as the new CEO effective March 1st — coming from HP, where he served as President and CEO.

This is where I need to be direct: my original thesis was built on the transformation vision that Alex Chriss articulated. A CEO who came from Intuit, who spoke the language of products and payment ecosystems, and who had begun laying the foundations for a modern commerce platform.

Lores is an excellent operational executive with a proven track record at HP, a company that navigated complex transformations with discipline and execution focus. But HP and PayPal are very different animals. One manufactures hardware in a mature market; the other competes in digital payments where speed of innovation and deep product understanding are critical.

The board justifies the change exclusively on execution grounds, not strategy, and Lores was involved in defining the guidance and priorities for 2026. That gives me some comfort, but it also raises a legitimate question: if the strategy is sound and Lores endorses it, what guarantees that a CEO from outside the payments industry can accelerate an execution that requires technical knowledge, deep relationships with global-scale merchants, and an understanding of digital consumer behavior? We don’t have that answer yet.

2026 Guidance: A Year of Investment Without a Clear Inflection

For 2026, management projects Non-GAAP EPS ranging from a low single-digit decline to slightly positive versus the $5.31 of 2025.

The ~3 percentage point headwind on Transaction Margin growth from strategic investments in checkout, BNPL, loyalty, and agentic commerce is a long-term bet that I understand and respect — but it also means 2026 will be a year of “faith” for the investor: believing that those investments will generate future acceleration without quantifiable near-term evidence.

And to complicate things further, the company explicitly withdrew the long-term outlook it had presented at the 2025 Investor Day, arguing that the environment proved more complex than anticipated.

Additionally, for Q1 2026, they expect Non-GAAP EPS to decline mid-single digits. The adjusted FCF guidance of ≥$6B and ~$6B in buybacks look solid from a shareholder return standpoint, but they don’t move the needle if the branded checkout inflection remains a promise without a timeline.

My Stance: I’ll Stay a Shareholder, but With a Smaller Position

Selling 40% of my position was not an emotional decision — it was a portfolio management decision. When an investment has a key catalyst (in this case, leadership and execution on branded checkout) and that catalyst changes unexpectedly, position sizing must reflect the increased uncertainty.

I remain bullish on the underlying assets: Venmo has real momentum, Enterprise Payments is demonstrating genuine pricing power, and the bet on agentic commerce with Perplexity, Microsoft Copilot, and the Cymbio acquisition points toward where payments are heading… but the clock on my thesis reset with the CEO change.

I now need to see evidence that Lores can execute at the speed this business requires, and that branded checkout shows a real improvement trajectory over the next two or three quarters.

PayPal remains an extraordinary company. But since investing isn’t about falling in love with a business — it’s about managing probabilities and risks — today the size of my position reflects exactly that: measured conviction while I wait for the data to confirm what the narrative still promises.

We’ll see what the next few quarters have in store. Until then.1

Disclaimer: This article reflects my personal investment strategy and opinions. I am not a financial advisor. Please do your own research before making any investment decisions.

A great CEO doesnt need to know the nuts and bolts of their industry. They just need to know who to listen to. The previous one was a bit thin on the ground when it came to communicating his vision to wall st. Hopefully the new one can articulate better